The Maurice Kilbride Market Intelligence Report - July 2026

What the National Property Market Is Telling Us

There is a slightly more cautious feel to the housing market as we move into July.

The first half of 2026 has not been weak, but it has become more selective. Buyers are still active, sellers are still coming to market, and well positioned homes are still selling — but the days of simply listing a property and expecting the market to do the work are long gone.

That is the important distinction. The market has not stopped. It has become more disciplined.

Buyers still have plenty of choice, they are taking longer to make decisions, and they are more willing to walk away if a property does not feel correctly priced.

For sellers, that creates a very clear message:

👉 Strategy matters more than ever

Before we look at what this means locally across Cheadle, Cheadle Hulme, Gatley, Edgeley and Cheadle Heath, it is worth looking at what the latest national house price indices are telling us.

UK House Prices – A Market That Is Holding, But Not Rushing Ahead

Most of the major indices are still pointing towards modest growth or broad stability rather than any sharp correction.

Rightmove’s June index put the average new seller asking price at £376,191, down 0.6% month-on-month and 0.5% lower year-on-year. Rightmove described this as the biggest June fall in 14 years, with stock still historically high despite being slightly down on last year.

Nationwide reported an average UK house price of £277,484 in June, with annual growth rising to 2.2%, up from 1.7% in May, although prices were broadly flat month-on-month.

Zoopla’s June House Price Index shows the average UK house price at £271,900, with annual growth of 1.4%, describing the market as one of modest growth supported by easing mortgage rates and resilient demand in many regions.

The latest ONS / Land Registry release, published in June, shows average UK house prices at around £270,000 in April 2026, up 3.8% over the previous 12 months. Because this is based on completed sales, it naturally lags behind the other indices.

Halifax’s latest available House Price Index showed the typical UK property at £298,806, with prices broadly stable and annual growth of 0.5%.

What the UK's Major House Price Indices Are Telling Us At A Glance

| Index | Average Price | Annual Change | Measures |

|---|---|---|---|

| Rightmove | £376,191 | -0.5% | Asking Prices |

| Halifax | £298,806 | +0.5% | Mortgage Approvals |

| Nationwide | £277,484 | +2.2% | Mortgage Approvals |

| Zoopla | £271,900 | +1.4% | Market Values |

| ONS / Land Registry | £270,000 | +3.8% | Completed Sales |

At first glance, these figures can look confusing.

Rightmove is showing asking prices softening. Nationwide is showing annual growth increasing. Zoopla is showing modest growth. The ONS is showing stronger annual growth, but from completed sales that lag the market.

But the reason is simple:

They are all measuring different stages of the property journey.

Rightmove measures what sellers are asking. Halifax and Nationwide reflect mortgage lending. Zoopla gives us a view of market values and agreed activity. ONS / Land Registry tells us what has actually completed, which is always my preference.

So rather than asking which figure is “right”, it is better to look at the direction of travel.

And the message is fairly clear:

👉 The market is stable, but buyers are price-sensitive.

Asking Prices Are Softening — And That Matters

One of the most important stories this month comes from Rightmove.

Asking prices fell by 0.6% in June, taking the national average to £376,191. That may not sound dramatic, but it is significant because June is usually a stronger month for pricing.

This tells us something important about seller expectations.

Earlier in the year, many sellers came to market with confidence. That was understandable. Buyer activity had improved, mortgage rates had eased slightly, and spring normally brings more movement.

But as the market has become more competitive, asking prices are now having to reflect buyer behaviour more closely.

In simple terms:

Sellers may still want strong prices.

But buyers are increasingly demanding evidence of value.

This is exactly where some properties begin to struggle. If a home launches too high, buyers now have enough choice to look elsewhere.

That does not mean a seller has to undersell.

It means the launch price has to create attention, confidence and competition.

Mortgage-Based Indices Show Buyers Are Still Active

While Rightmove is showing a softening in asking prices, Nationwide’s data suggests the market is still holding up.

Annual growth increased to 2.2% in June, although the monthly figure was broadly flat.

That is an important distinction.

It suggests buyers are still moving, but they are not necessarily pushing prices higher month after month.

Halifax tells a similar story, with prices broadly stable and annual growth modest at 0.5% in its latest available data.

So the picture is not negative.

It is just more measured.

Homes are still selling. Buyers are still getting mortgages. Transactions are still happening.

But the market is no longer forgiving poor pricing in the way it might have done during stronger periods.

Zoopla – Modest Growth, But A More Selective Market

Zoopla’s June data is useful because it sits somewhere between the asking price data and the completed sales data.

Its latest House Price Index shows UK prices up 1.4% year-on-year, with the average house price now around £271,900.

Zoopla’s wider commentary points to a market where affordability is gradually improving in some areas, but where activity remains uneven.

That feels very consistent with what we are seeing more generally.

There is demand. But it is not blind demand.

Buyers are comparing options. They are looking at value. They are watching how long properties have been on the market.

And they are far less likely to chase something that feels overpriced.

ONS / Land Registry – The Completed Sales Reality Check

The ONS / Land Registry data is always worth including because it reflects completed transactions rather than asking prices or mortgage approvals.

The latest release shows average UK house prices at around £270,000, up 3.8% annually in April 2026.

At first glance, that looks stronger than some of the other indices.

But we need to remember that completed sales data works on a delay.

A property completing in April may have been agreed months earlier, so it can reflect market conditions from late winter or early spring rather than what buyers are doing today.

That does not make it less useful. It simply means it should be read differently.

The completed sales data confirms there has been no collapse in values. But the more immediate indices show a market that is now more cautious and more selective.

Supply and Choice Remain the Big Story

[INSERT SUPPLY / BUYER CHOICE GRAPHIC HERE]

If there is one national trend sellers need to understand, it is this:

👉 Buyers have plenty of choice

Rightmove notes that the number of homes for sale remains historically high, even though available stock is slightly down on last year.

That changes the balance of power.

When buyers have more choice, they do not need to rush. They compare more. They ask more questions. They are less likely to stretch. And they become much quicker to dismiss a property if it does not feel right.

This is why the first few weeks of marketing are so important.

A well-positioned property can still generate strong early interest.

But an overpriced or poorly presented property can lose momentum quickly and once that happens, it becomes much harder to get back.

Mortgage Rates, Confidence and Buyer Psychology

Mortgage rates remain one of the biggest influences on buyer behaviour.

Rightmove reported that the average two-year fixed mortgage rate had eased to 5.07%, down from 5.18% the previous month.

That is helpful, but affordability is still stretched compared with the ultra-low-rate years.

Even a small change in monthly repayments can make buyers think carefully about what they offer.

This is why the psychology of buyers has changed so much.

They are still viewing. They are still offering.

But they are also:

- Comparing more properties

- Taking longer to decide

- Negotiating harder

- Focusing more on value

- Walking away if something does not feel right

This does not stop homes from selling.

But it does mean pricing mistakes are exposed much faster than before.

The Biggest Misconception Sellers Need To Avoid

One of the biggest mistakes in this market is assuming that a higher asking price creates a higher sale price.

It doesn’t work like that. In a market where buyers have limited choice, ambitious pricing can sometimes be absorbed. But in a market where buyers have options, overpricing often has the opposite effect.

It reduces early interest.

It weakens viewing numbers.

It makes the property sit.

And once buyers start asking, “Why hasn’t that sold yet?” the dynamic changes.

Instead of buyers competing for the property, the property starts competing for buyers.

That is exactly why strategy is so important.

Not just price -Strategy.

2026 Forecasts – Still Positive, But More Measured

The outlook for the rest of 2026 remains uncertain. Steady at best, rather than spectacular.

Zoopla continues to point towards modest annual growth, while Rightmove’s earlier forecast was for asking prices to rise by around 2% across 2026.

Nationwide’s latest figures also suggest the market is still edging forward annually, even if monthly movement remains flat.

So the national picture is not one of panic. It is one of adjustment.

After the volatility of recent years, the market is finding a more normal rhythm. But normal does not mean easy. It means sellers need to be realistic, prepared and strategic from the start.

What This Means For Sellers

When we pull all the national data together, the message is consistent.

The market is not weak, but it is selective.

Asking prices are softening in some areas. Mortgage-based indices show modest annual growth. Completed sales data confirms values have held up. But buyers are behaving more carefully.

For sellers, this means the launch matters.

The first few weeks are still when a property has the most visibility, the most curiosity and the best chance of creating momentum.

If the price, presentation and marketing are right, good homes can still perform extremely well. If they are wrong, the market is less forgiving.

So What Does This Mean for Cheadle?

National figures give us the direction of travel.

But property markets are always local. What is happening nationally is not always exactly what is happening in the SK8 and SK3 area.

That is why the local data matters.

As we move into the Cheadle section of this month’s update, the key question is:

Are we seeing the same pattern locally — selective buyers, careful pricing, and a growing gap between homes that sell and homes that struggle?

That is where the story gets really interesting for local home sellers and buyers.

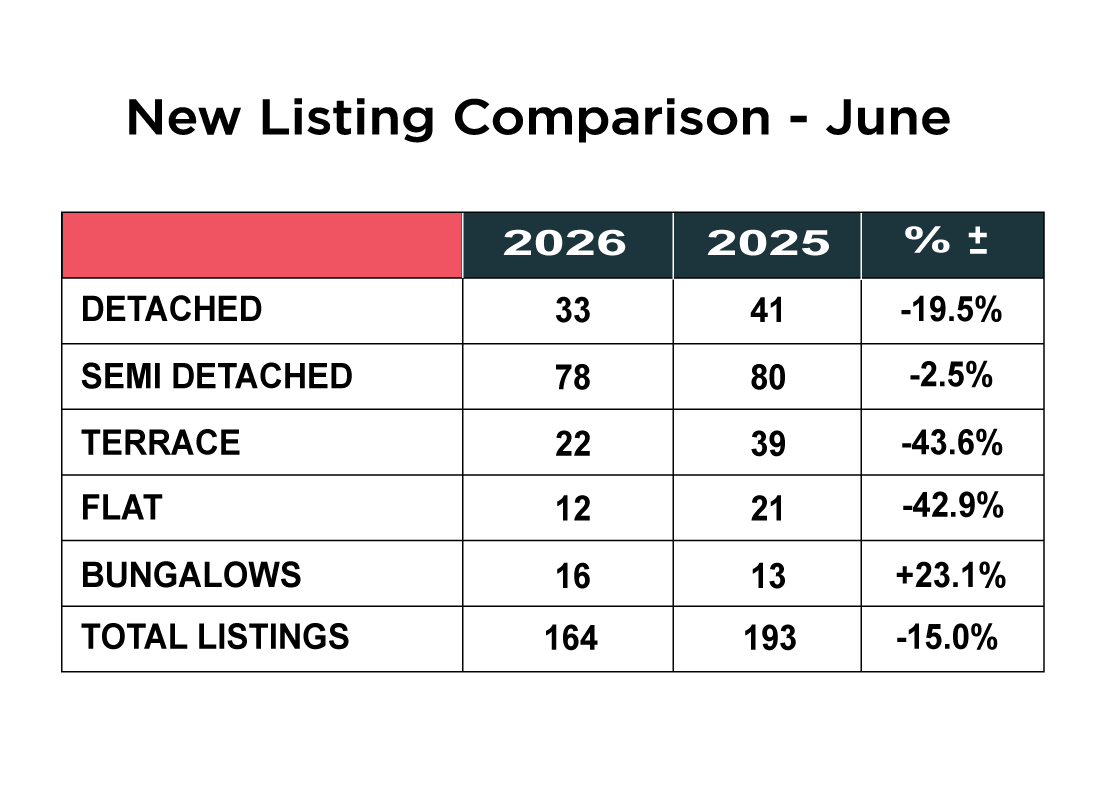

New Listings in SK8 & SK3 – Fewer Homes Coming to Market

One of the standout trends this month is the continued reduction in the number of homeowners choosing to bring their properties to the market.

Across SK8 and SK3, 164 properties were listed during June 2026, compared with 193 during the same period last year — representing a 15% reduction in new supply.

The most significant reductions have come in the terraced and flat sectors, with listings falling by 43.6% and 42.9% respectively. Detached homes have also seen fewer new instructions, down 19.5%, while semi-detached properties have remained relatively stable with only a modest 2.5% reduction.

Interestingly, bungalows continue to buck the trend, with new listings increasing by 23.1% year-on-year. While this is a relatively small sector of the market, it suggests that downsizers are becoming more active despite the wider shortage of available homes.

Overall, the figures suggest that although national headlines often focus on increasing supply, locally we're continuing to see fewer homeowners coming to the market than this time last year.

From our experience, when supply tightens and buyer demand remains healthy, correctly priced homes continue to attract strong early interest.

Key takeaway:

The number of new properties coming to market continues to fall locally, helping to maintain a healthy balance between supply and demand.

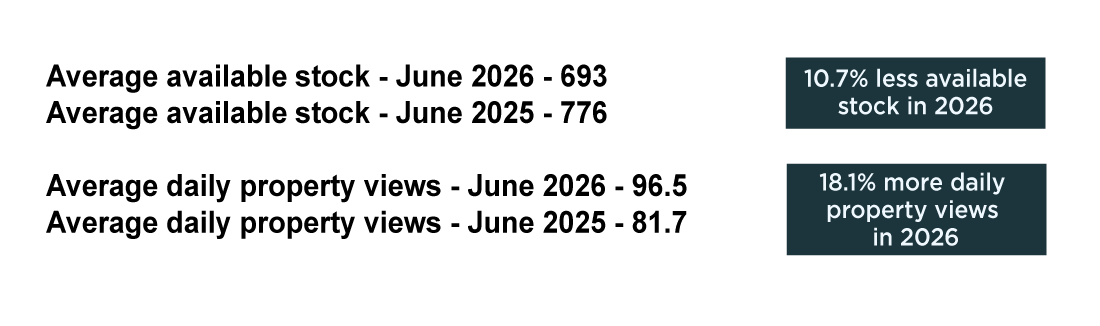

Stock Levels and Buyer Activity

While the number of new listings gives us one side of the story, it's the relationship between available stock and buyer activity that often provides the clearest picture of market conditions.

Across SK8 and SK3, the average number of homes available for sale during June stood at 693, compared with 776 during the same period in 2025 — a reduction of 10.7%.

At the same time, buyer engagement has strengthened considerably.

The average number of daily property views increased from 81.7 last year to 96.5 this June — an impressive 18.1% increase.

That combination is encouraging.

Fewer homes are available for buyers to choose from, yet more buyers are actively browsing the market than they were twelve months ago.

While buyers remain selective, the data suggests confidence has certainly not disappeared.

From our perspective, this continues to reinforce the importance of getting the launch strategy right from day one, when buyer interest is typically at its highest.

Key takeaway:

Buyer activity has increased significantly while available stock has reduced, creating favourable conditions for well-presented and realistically priced homes.

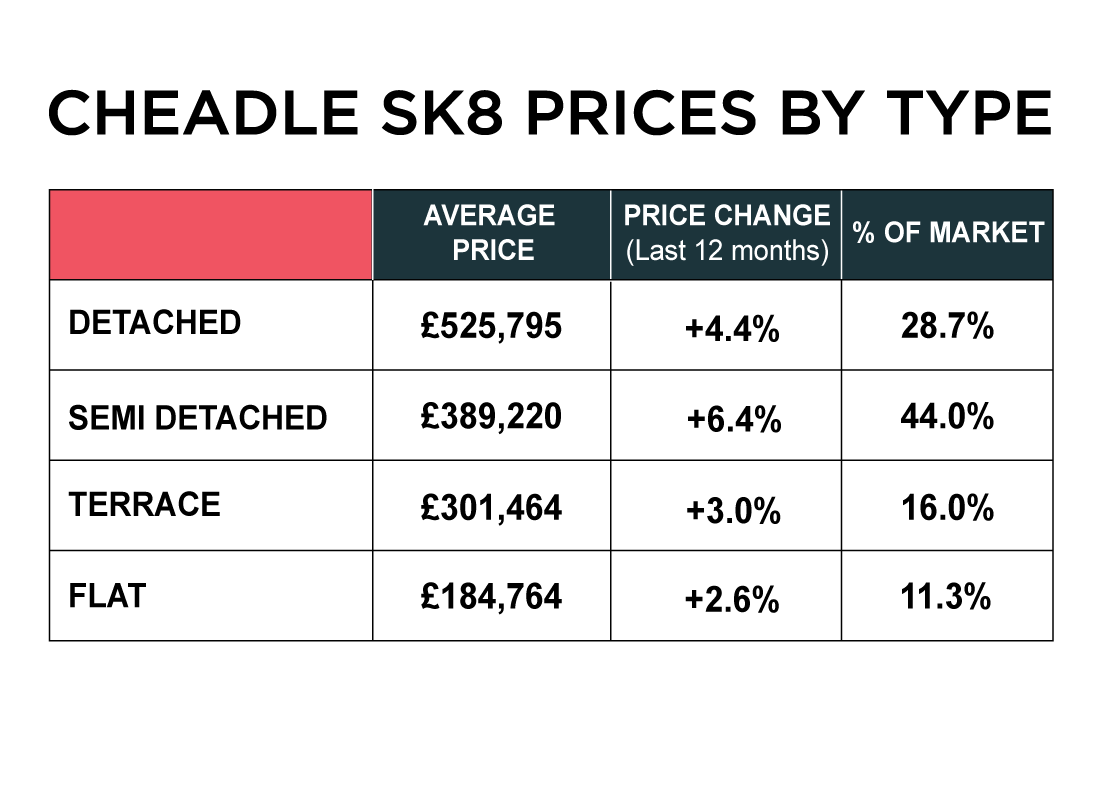

Property Prices in Cheadle (SK8)

Turning to the SK8 market, average property values have continued to show steady year-on-year growth across every property type.

Detached homes now average £525,795, representing annual growth of 4.4%, while semi-detached homes — which account for 44% of the local housing stock — have risen by 6.4% to an average of £389,220.

Terraced homes have also recorded modest growth, increasing 3.0% to £301,464, while flats have risen 2.6%, with average values now standing at £184,764.

Perhaps the most encouraging aspect of this month's figures is their consistency. Rather than one part of the market outperforming another, every property type has seen positive annual growth, suggesting a stable and well-balanced local market.

Key takeaway:

Property prices across SK8 continue to show steady, sustainable growth, with family homes remaining particularly resilient.

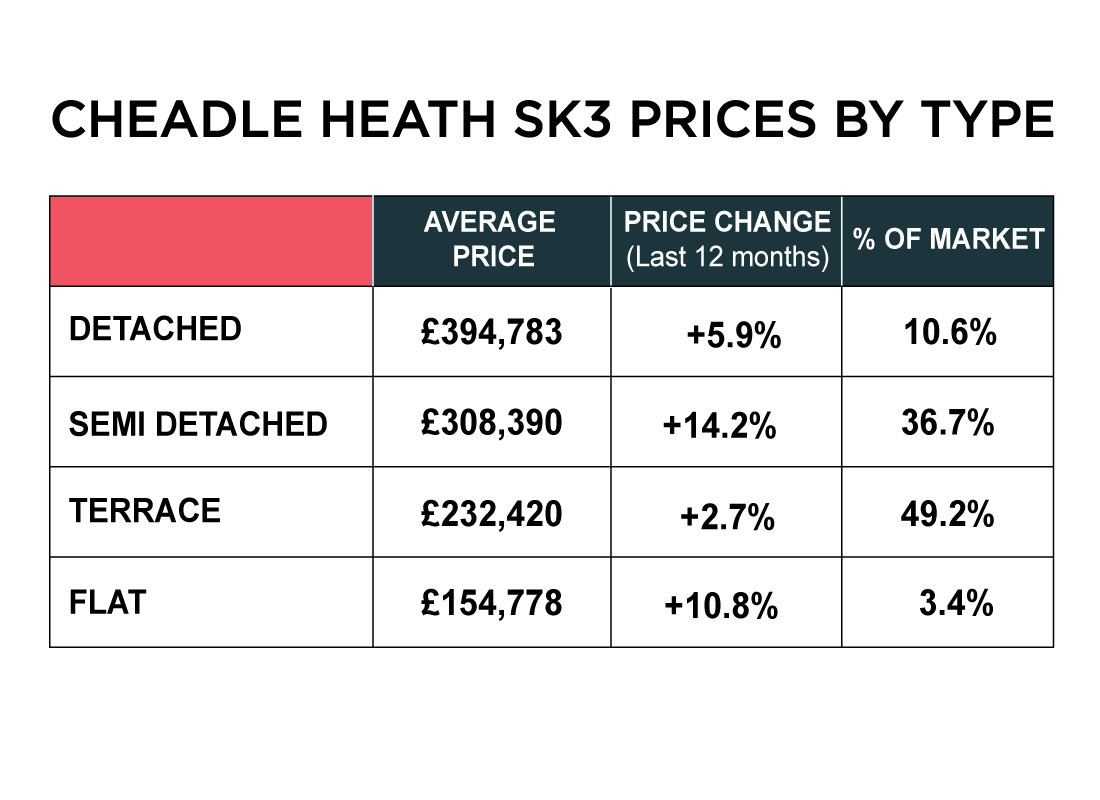

Property Prices in Cheadle Heath (SK3)

The SK3 market has also delivered another encouraging set of figures, with every property type recording positive annual price growth.

Detached homes now average £394,783, up 5.9% over the past year, while semi-detached properties continue to lead the way, rising 14.2% to an average of £308,390.

Terraced homes, which make up almost half of the local housing stock, have increased 2.7% to £232,420, while flats have performed particularly well, recording annual growth of 10.8%.

Taken together, these figures suggest demand remains strongest in the more affordable sectors of the market, with first-time buyers and growing families continuing to underpin local activity.

Key takeaway:

House prices across SK3 continue to move in a positive direction, particularly in the core family and first-time buyer sectors.

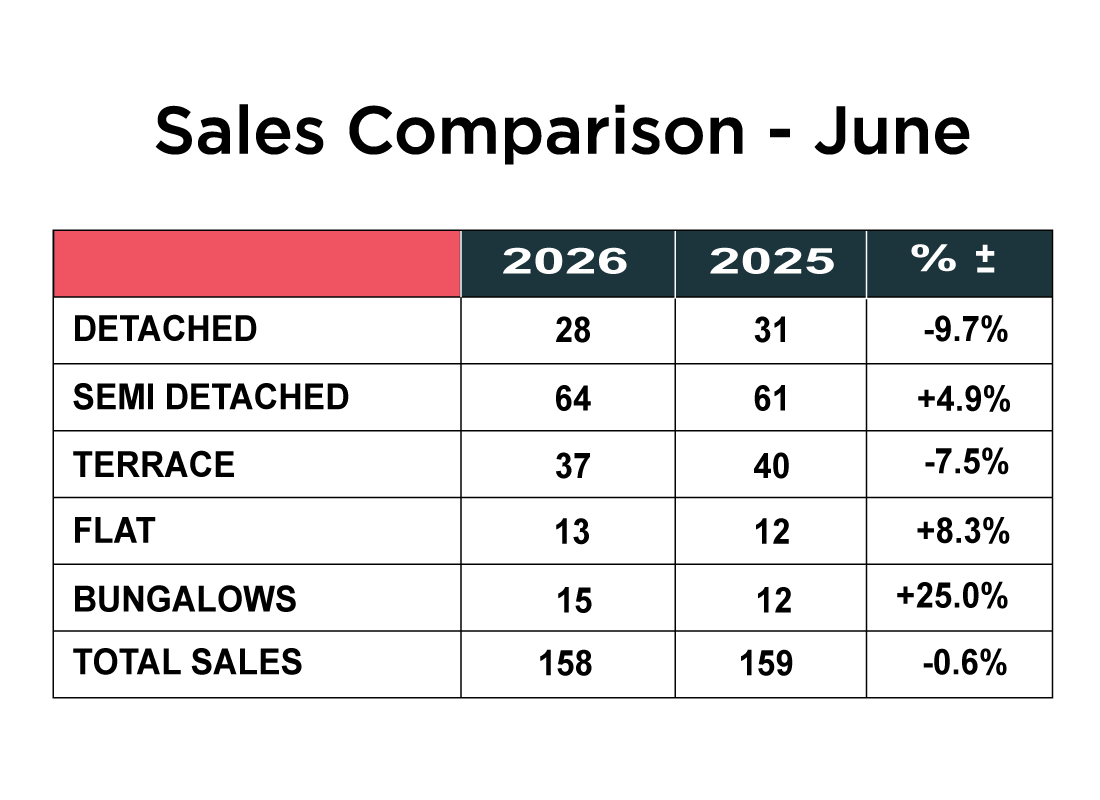

Sales Activity – A Stable Market Despite Lower Supply

Despite significantly fewer new properties coming onto the market this year, the number of agreed sales has remained remarkably consistent.

Across SK8 and SK3, 158 homes sold during June 2026, compared with 159 during the same period last year — a difference of just 0.6%.

Semi-detached homes continue to be the strongest-performing sector, with sales increasing by 4.9%, while bungalow sales have risen by 25%, reflecting continued demand from downsizers.

Detached sales have eased slightly, falling 9.7%, while terraced homes have dipped 7.5%. Flat sales, meanwhile, have edged upwards by 8.3%, albeit from a relatively small base.

What stands out most is not the individual movements between property types, but the overall resilience of the market. Despite fewer homes coming to market, buyers are continuing to transact at very similar levels to last year.

Key takeaway:

Although supply has tightened considerably, sales activity has remained stable, highlighting continued confidence amongst committed buyers.

Local Market Insight

When we step back and look across all of this month's data, a very clear picture begins to emerge.

Fewer homeowners are choosing to sell, which has reduced the amount of available stock across SK8 and SK3. At the same time, buyer activity has increased by more than 18%, suggesting there is still healthy demand from people looking to move.

House prices have continued to rise across virtually every property type, while the overall number of agreed sales has remained almost identical to last year, despite significantly fewer homes coming onto the market.

For us, this reinforces one message more than any other.

The market hasn't become easier or harder — it has become more strategic.

Homes that are priced correctly, presented well and launched with a clear marketing strategy continue to attract strong interest and achieve excellent results. Those that miss that crucial early window often find themselves chasing the market rather than leading it.

That's why we continue to believe that, in today's market more than ever, listing a property isn't enough — selling it requires a strategy.

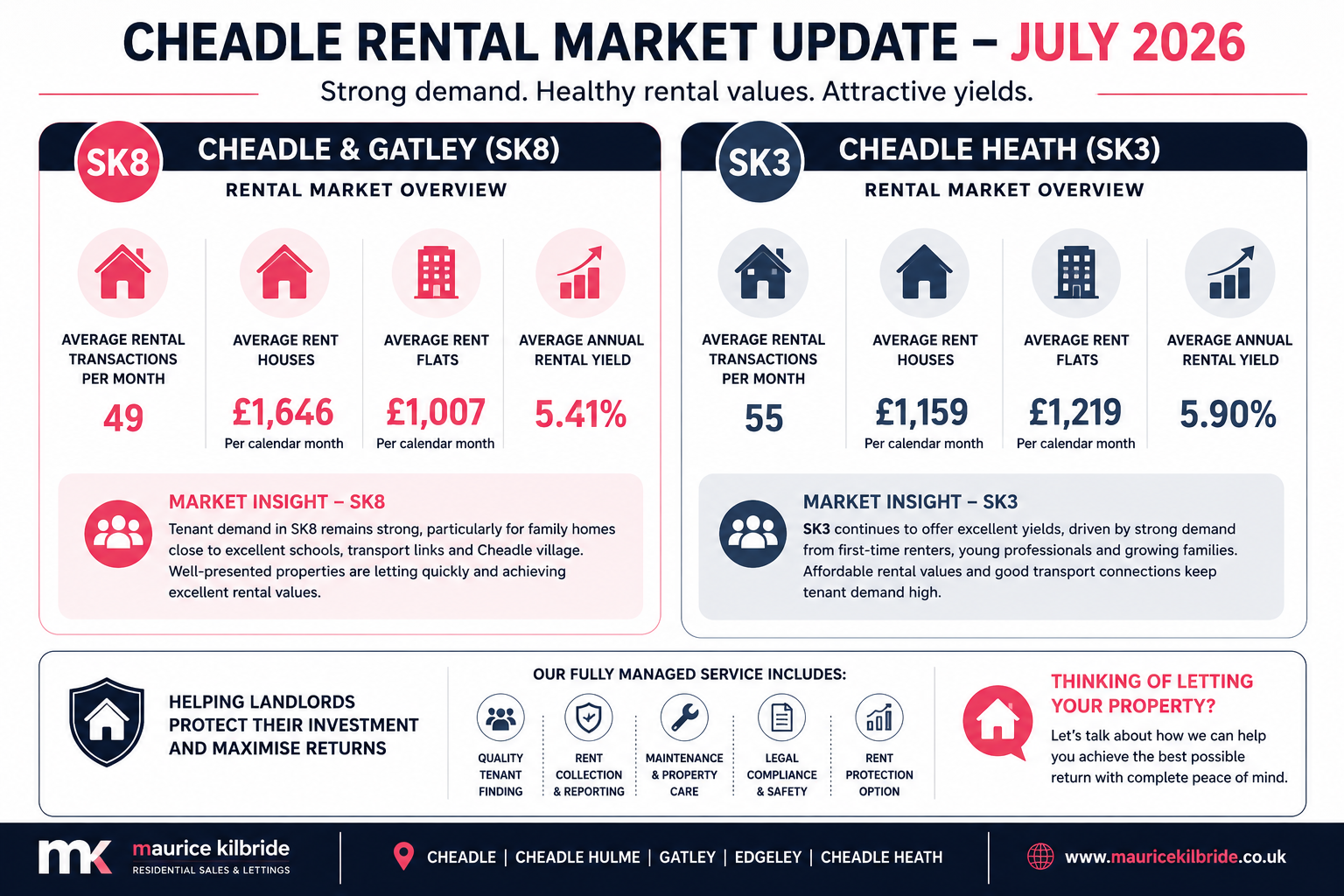

Cheadle Rental Market Update – July 2026

While the sales market often grabs the headlines, the local rental market has continued to perform strongly throughout 2026, with demand remaining resilient across both SK8 and SK3.

Following the introduction of the Renters' Rights Act in May this year, many landlords have understandably been reviewing their investment strategies. Although the legislation has introduced additional responsibilities, it has done little to dampen tenant demand locally, with well presented properties continuing to let quickly.

In SK8, the average rental transaction stands at 49 lets per month, with houses achieving an average rent of £1,646 per calendar month and flats averaging £1,007 per calendar month. Average gross rental yields currently stand at 5.41%, continuing to offer attractive long-term returns alongside the potential for capital growth.

Across SK3, activity remains equally encouraging. The area is averaging 55 rental transactions each month, with houses achieving around £1,159 per calendar month and flats averaging £1,219 per calendar month. Rental yields remain particularly attractive at 5.90%, reflecting the area's affordability and continued demand from first-time renters and young professionals.

Perhaps the most encouraging aspect of the local rental market is that demand continues to outstrip supply in many price brackets. Well presented properties, correctly priced and fully compliant with the latest legislation, continue to attract strong interest and quality applicants.

What Does This Mean for Local Landlords?

The introduction of the Renters' Rights Act has undoubtedly changed the way landlords need to manage their investments. Compliance is now more important than ever, and the administrative burden has increased.

However, the fundamentals remain positive.

Tenant demand across Cheadle, Cheadle Hulme, Gatley, Edgeley and Cheadle Heath continues to be strong, rental values remain healthy, and good quality properties are still letting quickly.

For landlords, success is no longer simply about finding a tenant. It is about protecting your investment, remaining compliant, minimising void periods and ensuring your property is positioned correctly in an increasingly regulated market.

Key takeaway:

Strong tenant demand, healthy rental yields and limited supply continue to make the local rental market attractive, provided landlords remain proactive and fully compliant with the latest legislation.

Thinking of Selling or Letting in 2026?

Whether you're considering selling your home or exploring the potential of your rental property, understanding the current market conditions is the first step towards making an informed decision.

Every property is different, which is why we create a tailored strategy for every client we work with. Whether your goal is to maximise your sale price or achieve the best possible rental return, our advice is always based on local market data, experience and a clear plan.

If you'd like to understand what your property could be worth — either for sale or to let, we'd be delighted to provide a confidential, no-obligation market appraisal.

Share this article

More Articles

Sign up for our newsletter

Subscribe to receive the latest property market information to your inbox, full of market knowledge and tips for your home.

You may unsubscribe at any time. See our Privacy Policy.